LOTM ran a number of silver stocks through a screening of LOTM filters to see what AI (GROK) would reply.

LOTM is looking for highest probability names for share price appreciation when the factors listed below are considered for the following silver miners mentioned. Our time frame is three to four-years.

FACTORS applied:

- A company’s growth potential

- Best value at today’s entry point of buying

- AISC number where appropriate.

- Has large scaled size of available portfolio properties to grow into.

- A number of fully diluted share count for share price leverage

- Has a reasonable debt level for projects and size of the opportunity

- Insider ownership is reasonable to be aligned with shareholder interest.

The results are provided at the end of this document. Here are the names provided for screening:

I. Production Stage: Generating Cash Flow

Focus: Producers with improving margins (AISC) and near-term production growth.

- Hecla Mining (HL)

- 2026 AISC: ~$15.00 – $16.25/oz.

- Shares: ~670 million.

- Market Cap: ~$11.55 billion.

- Thesis: Strongest primary producer growth in 2026 with Keno Hill ramp-up.

- Coeur Mining (CDE)

- 2026 AISC: ~$12.50 (Las Chispas) to $24.00 (Rochester).

- Shares: ~643 million.

- Market Cap: ~$11.35 billion.

- Thesis: Diversified production with massive leverage from the recent Rochester expansion.

- Aya Gold & Silver (AYASF)

- 2026 AISC: ~$14.50/oz.

- Shares: ~125 million.

- Market Cap: ~$2.1 billion.

- Thesis: Exceptional high-grade Moroccan asset with low share count relative to production scale.

- First Majestic Silver (AG)

- 2026 AISC: ~$20.90/oz (Consolidated).

- Shares: ~460 million.

- Market Cap: ~$7.9 billion.

- Thesis: Pure-play beta to silver price; significantly derisked via Cerro Los Gatos integration.

- Avino Silver & Gold (ASM)

- 2026 AISC: ~$25.00/oz (Projected to decrease).

- Shares: ~140 million.

- Market Cap: ~$150 million.

- Thesis: Deep value re-rating play as La Preciosa production triples output by 2028.

- Endeavour Silver (EXK)

- 2026 AISC: ~$22.00/oz.

- Shares: ~230 million.

- Market Cap: ~$4.4 billion.

- Thesis: High-growth mid-tier benefiting from the commercial ramp-up of the Terronera mine.

- Americas Gold and Silver (USAS)

- 2026 AISC: ~$17.70/oz.

- Shares: ~245 million.

- Market Cap: ~$3.3 billion.

- Thesis: Growth focused on the Galena Complex (USA) and the restart of the Crescent mine.

- GoGold Resources (GGD.TO / GLGDF)

- 2026 AISC: ~$18.00/oz.

- Shares: ~295 million.

- Market Cap: ~$650 million.

- Thesis: Stable producer in Mexico with massive growth potential from the Los Ricos development project.

- Santacruz Silver (SCZMF)

- 2026 AISC: ~$20.00 – $22.00/oz.

- Shares: ~340 million.

- Market Cap: ~$180 million.

- Thesis: High-leverage “turnaround” play with production normalizing across Mexico and Bolivia.

II. Developmental Stage: Advancing to Production

Focus: “Permitting to Construction” phase where the largest value re-ratings typically occur.

- Contango Silver & Gold (CTGO)

- Shares: ~30.5 million.

- Market Cap: ~$750 million.

- Thesis: Extremely low share count; transitioning from a gold focus to a major silver/gold producer via merger.

- Discovery Silver (DSVSF)

- Projected AISC: ~$12.50/oz.

- Shares: ~410 million.

- Market Cap: ~$420 million.

- Thesis: World-class scale; Cordero is the largest undeveloped primary silver project.

- Silver One Resources (SLVRF)

- Shares: ~205 million.

- Market Cap: ~$85 million.

- Thesis: Candelaria (Nevada) heap leach restart offers low-CapEx path to production.

- Hycroft Mining (HYMC)

- Shares: ~215 million.

- Market Cap: ~$450 million.

- Thesis: Massive optionality; sulfide technical studies represent a “binary” value catalyst.

- Vizsla Silver (VZLA)

- Shares: ~240 million.

- Market Cap: ~$410 million.

- Thesis: Panuco project is a top-tier high-grade development play in Mexico with aggressive drill success.

- Silver Mountain Resources (AGMRF)

- Projected AISC: ~$17.00/oz.

- Shares: ~195 million.

- Market Cap: ~$510 million.

- Thesis: Moving toward 2026 production at Reliquias (Peru); highly leveraged to silver/base metal mix.

- Silver Tiger Metals (SLVTF)

- Shares: ~360 million.

- Market Cap: ~$120 million.

- Thesis: Advancing the high-grade El Tigre project in Mexico; target for near-term PEA.

- Andean Silver (ASL.AX)

- Shares: ~180 million.

- Market Cap: ~$110 million.

- Thesis: High-grade focus on Cerro Bayo; consolidating assets for a centralized processing hub.

- Guanajuato Silver (GSVR)

- Shares: ~395 million.

- Market Cap: ~$95 million.

- Thesis: Consolidator of past-producing mines in Mexico; high operating leverage to silver price.

- Apollo Silver (APGO)

- Shares: ~190 million.

- Market Cap: ~$45 million.

- Thesis: Calico project (California) offers a large, simple pit-constrained resource in a safe jurisdiction.

III. Exploration Stage: Discovery & Resource Expansion

Focus: Drill-bit success and high-grade discovery in under-explored districts.

- Outcrop Silver (OCGDF)

- Shares: ~245 million.

- Market Cap: ~$60 million.

- Thesis: Consistent 1,000+ g/t AgEq intercepts; Santa Ana project is a “grade king” play.

- Summa Silver (SSVR)

- Shares: ~115 million.

- Market Cap: ~$55 million.

- Thesis: High-grade exploration in Mogollon (New Mexico) and Belmont (Nevada).

- Blackrock Silver (BRC.V / BKRRF)

- Shares: ~210 million.

- Market Cap: ~$65 million.

- Thesis: Tonopah West is one of the highest-grade undeveloped silver projects in Nevada.

- Reyna Silver (RSLV)

- Shares: ~165 million.

- Market Cap: ~$35 million.

- Thesis: Exploration focused on district-scale CRD (Carbonate Replacement Deposits) in Mexico.

- Silver Storm Mining (SVSTF)

- Shares: ~420 million.

- Market Cap: ~$50 million.

- Thesis: Revitalizing the past-producing La Parrilla mine complex; high resource growth potential.

- Kuya Silver (KUYAF)

- Shares: ~110 million.

- Market Cap: ~$40 million.

- Thesis: High-grade focus in Peru (Bethania) and Canada (Silver Kings).

- Silver X Mining (AGXPF)

- Shares: ~190 million.

- Market Cap: ~$45 million.

- Thesis: Improving operational efficiencies at the Nueva Recuperada district in Peru.

- Heliostar Metals (HST.V / HTXMF)

- Shares: ~195 million.

- Market Cap: ~$115 million.

- Thesis: High-grade gold-silver play in Mexico (Ana Paula) with a newly acquired silver production asset.

- Regency Silver (RSMXF)

- Shares: ~135 million.

- Market Cap: ~$25 million.

- Thesis: Speculative high-grade breccia discovery at Dios Padre in Mexico.

- First Andes Silver (FAS.V / MSLVF)

- Shares: ~95 million.

- Market Cap: ~$15 million.

- Thesis: Micro-cap high-grade discovery play in Peru; extremely low share count for high leverage.

RESULTS of the GROK SCREENING with LOTM FACTORS:

The highest-probability silver miners for share price appreciation over the next 3–4 years, based on the factors you specified, are primarily in the Production and Developmental stages. These offer a balance of improving cash flow/margins, clear execution paths (expansions or construction), strong balance sheets, and meaningful leverage via share count or undervaluation—without the binary risks of pure exploration plays. Exploration-stage names (e.g., Outcrop Silver, Summa Silver) have asymmetric upside on drill success but lower probability due to permitting, dilution, and execution risks.

GROK prioritized:

- Growth potential → Near-term production ramps or derisked projects advancing to cash flow.

- Best value at entry → Low market cap relative to resources/production scale and projected output (using your provided figures as baseline, cross-checked with latest public data).

- AISC → Lower = better margins as silver prices rise.

- Portfolio scale → Large resources or district potential for multi-year expansion.

- Fully diluted share count → Lower = greater price leverage on news/cash flow.

- Debt levels → Reasonable/manageable (low or net-cash positions preferred) relative to opportunity size.

- Insider ownership → Alignment (generally modest across the sector at 3–6% for these names, with some Canadian juniors historically higher via options/exercises; not a strong differentiator here but noted where relevant).

Latest data (as of ~March 2026) shows strong balance sheets industry-wide, with many producers/developers sitting on cash post-financings and reduced leverage. Silver price leverage remains the sector tailwind, but these stand out for operational derisking.

Top Recommendations (Ranked by Probability-Weighted Upside)

These combine your theses with updated financial health, debt, and insider metrics.

- Avino Silver & Gold (ASM) – Highest probability deep-value re-rating play

- Why top-ranked: Exceptional value at entry (your ~$150M market cap for a producer tripling output via La Preciosa by 2028). Near-zero debt (~$0.4M–$6M total, D/E ~0.2%; more cash than debt). AISC projected to decline from ~$25/oz as the ramp occurs. Low share count (~140M) provides strong price leverage. Portfolio growth via integration and Mexico assets.

- Fit to criteria: Massive growth potential with derisked path; best entry valuation among producers; improving margins; reasonable (negligible) debt for the scale; insider holdings ~5–6% (8M+ shares). High probability of re-rating as production triples and cash flow surges.

- Risk note: Execution on La Preciosa ramp; Mexico jurisdiction (familiar to many peers here).

- GoGold Resources (GGD.TO / GLGDF) – Best de-risked growth with fortress balance sheet

- Why high probability: Stable Mexican production + massive Los Ricos development (your thesis on growth potential). Zero/negligible debt (cash ~$141M–$245M USD post-financing; explicitly called out as “strong balance sheet, no debt”). AISC ~$18–24/oz range (recent actuals ~$23.72 but improving). Shares ~295M (moderate leverage). Large-scale Los Ricos project offers multi-year expansion.

- Fit to criteria: High growth from development project funded without dilution risk; attractive value vs. cash + assets; reasonable AISC; huge portfolio upside; debt-free for opportunity size; insider alignment via recent option exercises (historically ~25% range in sector peers). Excellent probability of steady appreciation as Los Ricos advances to construction/production.

- Risk note: Capital intensity of Los Ricos (~$227M feasibility capex, but fully funded).

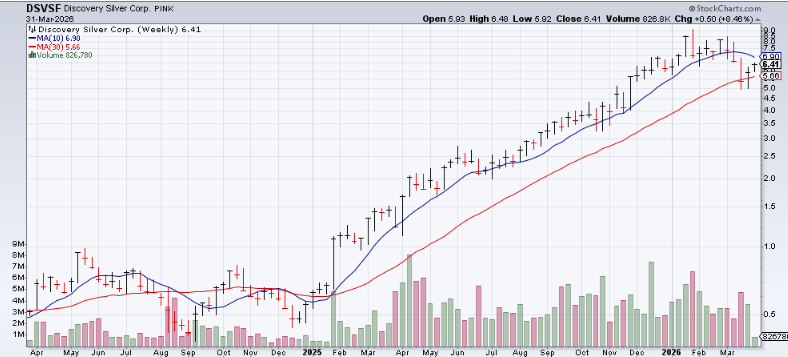

- Discovery Silver (DSVSF / DSV.V) – Top developmental re-rating candidate

- Why strong: World-class Cordero (your thesis: largest undeveloped primary silver project) with projected AISC ~$12.50/oz. Low debt (~$6.6M, D/E ~1%). Shares ~410M but very low market cap (~$420M) relative to scale = high leverage on permitting/construction news. Portfolio is district-scale with expansion potential.

- Fit to criteria: Highest growth potential in “permitting to construction” phase (biggest value re-ratings occur here); attractive value for the resource size; best-in-class AISC; enormous portfolio to grow into; debt is minimal for the opportunity. Insider data limited but typical junior alignment. Highest-probability developer for 3–4 year upside as it derisks toward production.

- Risk note: Permitting timeline; shares higher than pure low-float plays.

- Aya Gold & Silver (AYASF / AYA.TO) – High-grade growth with leverage

- Why competitive: Low AISC (~$14.50/oz), exceptional Moroccan assets (your high-grade thesis), recent record results/revenues. Debt moderate (~$113M, D/E ~28–29%; cash ~$129M). Shares ~142M (slightly higher than your ~125M). Strong portfolio scale.

- Fit to criteria: Excellent growth potential; solid value; attractive AISC; large high-grade assets to expand; debt reasonable relative to cash flow growth. Insider ~3.5%. Good probability in production stage.

- Risk note: Shares increased; debt higher than top picks (though serviceable).

Other Notable Mentions (Lower Probability or Higher Risk/Reward)

- Hecla Mining (HL): Strongest primary producer growth (Keno Hill ramp-up), low AISC (~$15–16/oz), reduced debt (~$270M, D/E ~10%). Large scale but high shares (~670M) and market cap (~$11.55B) limit leverage. More stable blue-chip play, lower % upside probability.

- Vizsla Silver (VZLA): High-grade Panuco (top-tier dev), now funded via convertible notes (~$240M raised, cash >$450M). Debt present but project-specific. Insider ~5.4%. Strong growth but higher leverage/risk than top picks.

- Contango Silver & Gold (CTGO): Extremely low shares (~30–32M post-merger) = massive leverage. Debt repaying (plans debt-free 2027). Silver/gold shift via merger, but higher execution risk and current D/E.

Pure exploration plays (e.g., Outcrop, Summa, Blackrock, First Andes) score lower on probability due to discovery/permitting risks, even with low shares/mcaps and high-grade potential. They require drill success for meaningful appreciation.

Overall sector context: These names benefit from improving AISC (All in Sustaining Costs) guidance, production ramps, and low-to-moderate debt in a rising silver environment. Low share count + derisked growth + strong BS = highest probability of outsized appreciation vs. larger or higher-debt peers. ASM and GoGold stand out for value + leverage + balance sheet strength. DSVSF for scale in development. Monitor quarterly updates on AISC, production guidance, and permitting.

This is an analytical assessment based on your listed factors and publicly available data—not investment advice. Markets and projects evolve; verify latest filings, resource estimates, and silver price assumptions for your entry. GROK, over and out.

LOTM (Tom) believes the Silver, Copper, and Gold markets will remain strong for three to five more years due to ongoing supply shortages. Commodity bull markets are shaped by supply and demand; once supply increases, mining activity slows and the market cycle ends. From 2011 to 2021, miners faced underinvestment, and bringing new production online is a lengthy process—often spanning decades. Copper’s supply gap may persist even longer than those for silver or gold.

Two-year charts of the four highest rated companies.

Warning or be aware, however you might consider your risk factor.

- Three of the above companies operate in Mexico. ASM, GLGDF, and DSVSF are all in Mexico.

- Aya Gold and Silver is in Morocco

Silver Prices reacted positively on March 31 2026 below

LOTM Research & Consulting Service

* An account related to LOTM holds a position in this security.

Neither LOTM nor Tom Linzmeier is a Registered Investment Advisor.

Please refer to our web site for full disclosure at www.LivingOffTheMarket.com ZTA Capital Group, Inc.

To Unsubscribe please select “return” and type Unsubscribe in the subject line..

![]()