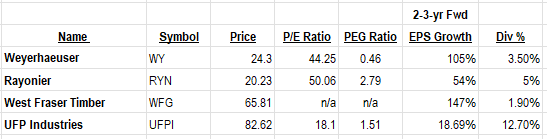

Comparative Review of WY, RYN, WFG and UFPI

Prepared for Long-Term (3-year) Investors

Executive Summary

LOTM is focused on Crypto/AI related companies and Physical Mining Companies. We want to add a third investment leg that is not correlated to Crypto or AI to reduce volatility. The forestry industry is cheap, I mean CHEAP. This report reviews four companies operating within the timber, forest products, and wood-products industry. The goal is to evaluate potential price appreciation, dividend characteristics, balance-sheet strength, cyclical opportunity, and strategic positioning over a three-year outlook. Our goal is a double or better in three years or less.

The sector is out of favor & appears to be in Stage 1 Basing chart pattern

Weyerhaeuser (WY)

Investment Role: Institutional-quality timberland and real-asset leader

Pros

- Largest and most diversified timber REIT in North America

- Massive land ownership base with long-term scarcity value

- Exposure to housing recovery and lumber demand

- Strong institutional ownership and financial strength

- Additional upside from carbon credits and climate solutions

Cons

- More sensitive to housing-cycle weakness

- Not likely to be the fastest-moving stock in the group

- Dividend yield lower than some peers

Strategic View: WY appears best suited for investors seeking a lower-risk, long-duration hard-asset holding. The company combines real estate, timber, and industrial exposure in a way that may provide steady appreciation during inflationary or lower-rate environments.

Three-Year Outlook: Estimated 3-year appreciation potential: +35% to +100% depending on housing and timber cycles.

Rayonier (RYN)

Investment Role: Higher-beta timber REIT with merger-driven upside

Pros

- Attractive dividend profile

- Lower valuation metrics compared to peers

- Potential re-rating from strategic merger scale benefits

- Greater upside torque during timber recovery cycles

Cons

- Higher operational and integration risk

- More cyclical earnings profile

- Smaller financial cushion than WY historically

Strategic View: RYN may offer a stronger percentage upside than WY if timber pricing improves and synergies from scale expansion are realized. The stock fits investors seeking a combination of income and cyclical appreciation potential.

Three-Year Outlook: Estimated 3-year appreciation potential: +40% to +120%.

West Fraser Timber (WFG)

Investment Role: High-risk, high-reward cyclical upside opportunity

Pros

- Strong leverage to lumber-price recovery

- Historically capable of explosive rebounds

- Operational leverage can significantly expand profits during housing upcycles

- Lower valuation compared to many industrial peers

Cons

- More volatile than WY or RYN

- Highly dependent on housing demand and lumber pricing

- Can experience sharp earnings swings

Strategic View: WFG represents the aggressive upside component of the sector. If rates decline and housing demand normalizes, WFG could potentially become the strongest performer in the group.

Three-Year Outlook: Estimated 3-year appreciation potential: +50% to +250% in a strong cyclical recovery.

UFP Industries (UFPI)

Investment Role: Operational compounder and disciplined industrial manager

Pros

- Strong management reputation

- Operational efficiency and disciplined execution

- Less speculative and more process-oriented

- Long-term compounder characteristics

Cons

- Less dramatic upside than WFG during commodity spikes

- Lower excitement factor for momentum-oriented investors

- More tied to execution than pure asset appreciation

Strategic View: UFPI may appeal to investors seeking a quieter but disciplined industrial compounder. The company combines manufacturing and wood-products exposure with operational consistency.

Three-Year Outlook: Estimated 3-year appreciation potential: +30% to +80%.

Final Perspective

For investors seeking lower correlation to crypto and AI, the timber and forest-products sector offer exposure to hard assets, productive land, biological (tree) growth, inflation protection, and potential institutional rotation into real assets. A blended strategy involving institutional leaders alongside a higher-risk cyclical upside candidate may provide an attractive balance between stability and asymmetric return potential.

It is LOTM’s perspective that the rotation into hard assets has three to five years of receiving money in-flows with diminishing money out-flows. Potentially a boring way to make 50 to 100% return over the next one to four years. Timing is the most difficult variables in the market to forecast.

LOTM Research & Consulting Service

* An account related to LOTM holds a position in this security.

Neither LOTM nor Tom Linzmeier is a Registered Investment Advisor.

Please refer to our web site for full disclosure at www.LivingOffTheMarket.com ZTA Capital Group, Inc.

To Unsubscribe please select “return” and type Unsubscribe in the subject line..

![]()