Prepared June 16, 2026, by Tom at LOTM

Companies:

- Silver One (SLVRF) $0.32

- Blackrock Silver (BKRRF) $0.79

- Outcrop Silver (OCGSF) $0.32

- Discovery Silver (DSVSF) $6.43

- Impact Silver (ISVLF) $0.24

- Vizsla Silver (VZLA) $3.65

- GoGold Resources (GLGDF) $2.41

The Ideas in this writing are Speculative, long-term and illiquid. They are similar to Venture Capital style positions.

INVESTMENT BRIEF: SILVER EQUITIES STRATEGY (2026–2030)

Prepared for: Private Portfolio Analysis

Focus Assets: SLVRF, BKRRF, OCGSF, DSVSF, IPT, VZLA, GGD

Time Horizon: 2-to-3-Year Core (Extended to 2030)

Strategy Profile: Defensive 60% Producer Anchor with High-Beta Options

1. CORE ASSET RISK-REWARD ANALYSIS

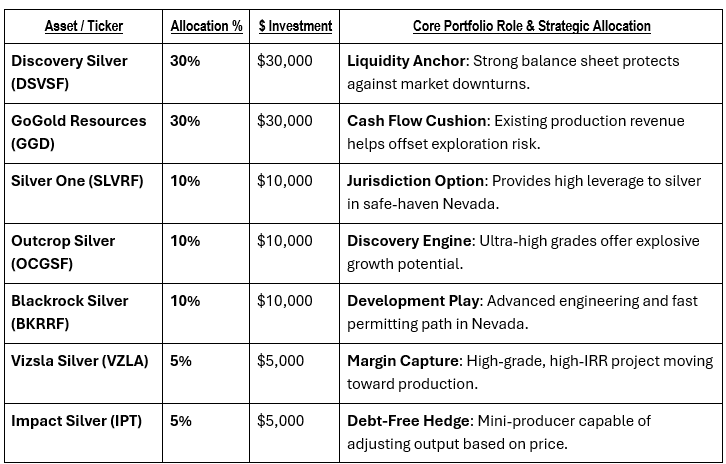

Silver One Resources Inc. (SLVRF)

- The Thesis: A highly leveraged, speculative play on silver demand. Its flagship Candelaria project in Nevada provides large scale, located in a secure Tier-1 mining jurisdiction.

- Pros & Milestones: Backed by a strong $32M capital position, the company launched a massive 25,000-meter drilling program to expand its 108M oz resource base. It is targeting a Pre-Feasibility Study (PFS) by late 2026/early 2027.

- Cons & Structural Risks: Zero near-term cash flow makes it vulnerable to timeline extensions. The historic heap leach pads are low-grade (~42.1 g/t Ag), making project viability highly dependent on achieving 59%–69% metallurgical recovery rates via its non-cyanide extraction technologies.

Blackrock Silver (BKRRF)

- The Thesis: An advanced developer leading on the engineering curve in Nevada. Its updated Preliminary Economic Assessment (PEA) shows a strong $437M after-tax NPV at base prices.

- 3-Year Track: Fast-tracking permitting to target a formal underground construction decision by H2-2027. This positions it as the closest developer to near-term cash flow, though its $21M annual burn rate requires ongoing capital management.

Outcrop Silver (OCGSF)

- The Thesis: A high-risk, high-reward explorer chasing world-class discovery potential in Colombia.

- 3-Year Track: Capitalizing on ultra-high-grade silver veins averaging 614 g/t AgEq. Utilizing a 4-rig drilling program to expand its resource base toward a 100M oz target ahead of its maiden PEA, though it remains exposed to regional political risk.

Discovery Silver (DSVSF)

- The Thesis: An advanced developer backed by a robust balance sheet.

- 3-Year Track: Boosted by recent asset additions, it holds $634.9M in total liquidity and reported a 25% jump in net income to $81.7M in Q1 2026. Deploying capital to scale up its production footprint and build out its world-class Cordero asset.

Impact Silver (IPT)

- The Thesis: A debt-free, pure-play producer driving organic growth from its operating mines.

- 3-Year Track: Leveraged strong silver prices and high grades at Zacualpan to triple Q1 2026 revenue to $31.2M. Using $45M in cash and recent high-grade discoveries at Noche Buena to scale throughput organically without dilutive equity raises.

Vizsla Silver (VZLA)

- The Thesis: Transitioning from mine design directly into active construction at its Panuco project in Mexico.

- 3-Year Track: Backed by a Feasibility Study boasting a 111% IRR, the company has awarded its Equipment Supply Agreement to FLSmidth to lock in long-lead mine machinery, funded via a dedicated government working capital facility.

GoGold Resources (GGD)

- The Thesis: A well-funded producer executing a major development build in Mexico.

- 3-Year Track: Generates $65M annually in free cash flow from its Parral tailings project and holds $261M in the bank with zero debt. With final environmental approvals secured, the company is building the Los Ricos South mine to grow annual output to 9.4M oz AgEq.

2. MACRO SCENARIO ASSUMPTIONS (BY 2030)

- Bear Case (30% Probability): Silver stabilizes at $22.00–$24.00/oz due to a global economic slowdown. High-burn explorers face severe equity dilution or project delays.

- Base Case (50% Probability): Silver stabilizes at $35.00–$42.00/oz, supported by sustained industrial and green energy demand. Advanced developers transition to mid-tier producers.

- Best Case (20% Probability): Silver spikes past $75.00+/oz in a commodities super-cycle. Exploration success drives exponential, multi-bagger valuation re-ratings.

3. CONSERVATIVE-LEAN PORTFOLIO WEIGHTING MODEL

Total Capital Investment: $100,000

4. CONSERVATIVE PORTFOLIO PERFORMANCE PROJECTIONS

- Bear-Case Outcome (30% Prob): Portfolio value falls to $74,250 (-25.75%). Capital loss is minimized by the $60,000 anchor allocation in liquid, zero-debt producers.

- Base-Case Outcome (50% Prob): Portfolio value rises to $231,250 (+131.25%). Growth is driven by Blackrock, Vizsla, and GoGold successfully executing their mine construction plans.

- Best-Case Outcome (20% Prob): Portfolio value rises to $565,000 (+465.00%). Speculative tranches in Silver One and Outcrop generate substantial gains during a metal breakout.

- Risk-Adjusted Expected Value: $250,900 (+150.90% Net Expected Return).

5. SECTOR CORRELATION & BEHAVIORAL MATRIX

- Systemic Liquidity Events: During broad market corrections, sector correlation spikes near +0.90. Fund selling overrides individual company fundamentals, causing high-grade producers and micro-cap explorers to decline simultaneously.

- Jurisdiction Rotation: Legal, regulatory, or tax changes in Mexico break standard correlations. Capital frequently rotates out of Latin America into safe-haven assets, benefiting Nevada-based assets like Silver One and Blackrock Silver.

- Commodity Breakout Decoupling: In the initial stages of a silver bull market, capital favors large, liquid producers (Discovery, GoGold). As valuations expand, capital rotates down into micro-cap assets, driving isolated, high-torque gains for Silver One and Outcrop.

By 2030, current exploration projects will have transitioned to advanced development or production, while existing producers will be at peak capacity or facing reserve depletion.

Key Macro Assumptions for 2030

- Bear Case (30% Probability): Global recession or technological substitution dampens industrial silver demand. Physical silver drops and stabilizes around $22.00 to $24.00/oz.

- Base Case (50% Probability): Continued green energy expansion (solar photovoltaics and electric vehicles) maintains a structural deficit. Physical silver stabilizes around $35.00 to $42.00/oz.

- Best Case (20% Probability): Severe global monetary debasement combined with unprecedented industrial shortfalls triggers a secular commodities super-cycle. Physical silver spikes and holds above $75.00+/oz.

Comparative 2030 Price Appreciation Potential

The rankings below represent the estimated percentage upside potential from current 2026 price levels to 2030 target targets, organized by economic scenario.

1. Best-Case Scenario Rankings (Secular Silver Bull & Maximum Upside)

This scenario favors early-stage, highly leveraged explorers and developers where discovery success and multi-million-ounce resource growth trigger exponential re-ratings.

- Outcrop Silver (OCGSF)

- Potential Appreciation: +900% to +1,200%

- Probability: 20%

- Catalyst: Proving up an ultra-high-grade (+600 g/t AgEq) system exceeding 150 million ounces in Colombia during a high-commodity market environment.

- Silver One Resources (SLVRF)

- Potential Appreciation: +700% to +950%

- Probability: 20%

- Catalyst: Successful pilot-scale metallurgical implementation on the Candelaria heap pads, turning a 108M oz low-grade bulk project into a highly profitable, low-cost USA asset.

- Blackrock Silver (BKRRF)

- Potential Appreciation: +600% to +800%

- Probability: 20%

- Catalyst: High-grade underground production execution at Tonopah West combined with aggressive deep exploration success.

- Vizsla Silver (VZLA)

- Potential Appreciation: +450% to +600%

- Probability: 20%

- Catalyst: Full scale-up of the Panuco EPCM facility to peak throughput under highly favorable margin metrics.

- GoGold Resources (GGD)

- Potential Appreciation: +300% to +450%

- Probability: 20%

- Catalyst: Seamless combination of Parral cash flows with a fully optimized Los Ricos South operation.

- Discovery Silver (DSVSF)

- Potential Appreciation: +250% to +350%

- Probability: 20%

- Catalyst: Large-scale commercial scaling of its premier assets backed by its dominant balance sheet liquidity.

- Impact Silver (IPT)

- Potential Appreciation: +200% to +300%

- Probability: 20%

- Catalyst: High-grade discoveries at Zacualpan and a complete, low-capex restart of Capire.

2. Base-Case Scenario Rankings (Steady Progression & Solid Metal Prices)

This scenario rewards companies transitioning predictably into production or significantly de-risking their economics through advanced engineering studies.

- Blackrock Silver (BKRRF)

- Potential Appreciation: +250% to +350%

- Probability: 50%

- Catalyst: Transition from an advanced PEA stage into a fully permitted, mid-tier underground mine builder in safe-haven Nevada.

- Vizsla Silver (VZLA)

- Potential Appreciation: +200% to +300%

- Probability: 50%

- Catalyst: Transitioning from the current FLSmidth equipment layout stage directly into commercial production at Panuco.

- GoGold Resources (GGD)

- Potential Appreciation: +175% to +250%

- Probability: 50%

- Catalyst: Bringing the newly permitted Los Ricos South mine online, increasing annual output to over 9.4M oz AgEq.

- Silver One Resources (SLVRF)

- Potential Appreciation: +150% to +225%

- Probability: 50%

- Catalyst: Publication of a definitive Pre-Feasibility Study (PFS) confirming stable economic recoveries via non-cyanide metallurgy.

- Discovery Silver (DSVSF)

- Potential Appreciation: +125% to +175%

- Probability: 50%

- Catalyst: Direct utilization of its major liquidity pile to advance large-scale project construction.

- Outcrop Silver (OCGSF)

- Potential Appreciation: +100% to +175%

- Probability: 50%

- Catalyst: Publication of its maiden PEA on Santa Ana showing strong economics despite regional Colombian country discounts.

- Impact Silver (IPT)

- Potential Appreciation: +75% to +125%

- Probability: 50%

- Catalyst: Sustained organic production growth funded entirely through existing operating cash flows.

3. Bear-Case Scenario Rankings (Market Downturn & Capital Preservation)

In a prolonged downturn, early-stage explorers suffer severe losses due to capital starvation. Producers with strong balance sheets and existing operations perform best on a capital-preservation basis.

- Discovery Silver (DSVSF)

- Potential Appreciation / Downside: -10% to +20%

- Probability: 30%

- Defense: Massive asset value cushion and excellent balance sheet liquidity protect it from structural impairment.

- GoGold Resources (GGD)

- Potential Appreciation / Downside: -20% to +10%

- Defense: Insulated by ongoing free cash flow from its existing Parral tailings operation and a large cash reserve.

- Impact Silver (IPT)

- Potential Appreciation / Downside: -30% to -10%

- Defense: Its zero-debt profile and ability to high-grade its operating mines allow it to weather low-price environments without dilutive financings.

- Vizsla Silver (VZLA)

- Potential Appreciation / Downside: -45% to -25%

- Defense: High-grade dynamics protect the project core, but low metals prices would delay its construction financing timeline.

- Silver One Resources (SLVRF)

- Potential Appreciation / Downside: -60% to -40%

- Defense: The $32 million cash cushion prevents immediate bankruptcy or severe dilution, but low-grade projects lose economic viability when silver drops.

- Blackrock Silver (BKRRF)

- Potential Appreciation / Downside: -65% to -50%

- Risk: High annual cash burn rates become dangerous if capital markets dry up during a mining bear market.

- Outcrop Silver (OCGSF)

- Potential Appreciation / Downside: -80% to -60%

- Risk: Jurisdictional risk combined with capital starvation would likely force highly dilutive equity raises to keep operations going.

The 2030 Portfolio Strategy Takeaway

- For Maximum Growth Potential: A barbell allocation putting capital into Outcrop Silver and Silver One offers the highest theoretical returns by 2030, but you must accept the risk of severe downside if a bear market occurs.

- For Optimal Risk-Adjusted Return: Focus your capital on Blackrock Silver and Vizsla Silver for the base-case scenario, or anchor your portfolio with GoGold and Discovery Silver for safety across all market conditions.

Excerpt from Canadian Mining Report below:

Why Analysts Believe Investing in Silver Is a Smart Move Right Now

May 13, 2026, Author – Ben McGregor

Silver Price Forecast 2026 and Silver Market Outlook

The silver price forecast for 2026 is increasingly constructive among analysts. UBS’s $100 target implies meaningful upside from current levels around $85/oz.

Other forecasters echo this view, citing:

- Industrial Demand Growth: Solar photovoltaic installations, electronics, and 5G infrastructure are driving steady consumption growth. Silver’s unique conductivity makes it difficult to substitute in many high-tech applications.

- Monetary and Investment Demand: Silver benefits from gold’s safe-haven flows while offering additional leverage through its industrial component. Investor positioning remains relatively light, suggesting room for further inflows.

- Supply Constraints: Mine production growth is limited, and above-ground stocks are being drawn down in key locations. Recycling provides some buffer but cannot fully offset primary supply tightness.

- Gold-Silver Ratio Dynamics: The ratio remains elevated by historical standards, supporting the view that silver could outperform gold on a relative basis (silver vs gold investment) if industrial demand accelerates.

The silver market outlook for 2026 points to a tightening balance, with potential for volatility around short-term flows but a structurally bullish trend driven by the energy transition and monetary diversification.

Reasons to Invest in Silver in 2026

There are several compelling reasons to invest in silver right now:

- Dual Demand Drivers: Silver’s unique position as both a monetary metal (like gold) and a critical industrial input provides a powerful combination in the current macro environment.

- Energy Transition Tailwinds: The solar boom and electrification trends are structural, not cyclical, supporting long-term demand growth.

- Undervalued Relative to Gold: The gold-silver ratio suggests silver offers attractive leverage if the ratio normalizes lower during a precious metals bull market.

- Supply-Demand Imbalance: Limited new mine supply and declining grades at existing operations create a favorable backdrop for higher prices.

- Investor Sentiment Shift: As gold reaches new highs, capital is rotating into silver for additional upside potential.

These factors support a positive silver investment outlook for 2026 for both physical silver and silver stocks.

Accounts related to LOTM may and will buy and sell names in this report at anytime and without notice to readers.

LOTM Research & Consulting Service

* An account related to LOTM holds a position in this security.

Neither LOTM nor Tom Linzmeier is a Registered Investment Advisor.

Please refer to our web site for full disclosure at www.LivingOffTheMarket.com ZTA Capital Group, Inc.

To Unsubscribe please select “return” and type Unsubscribe in the subject line

![]()