Past is the Past, We only Look Forward – common saying of Vietnamese people and a cornerstone in their culture

The next year is very bright for both Equinox Gold (EQX*) and B2Gold (BTG*)

Skate to where the puck will be, not to where it is – Attributed to Wayne Gretzky, former hockey great.

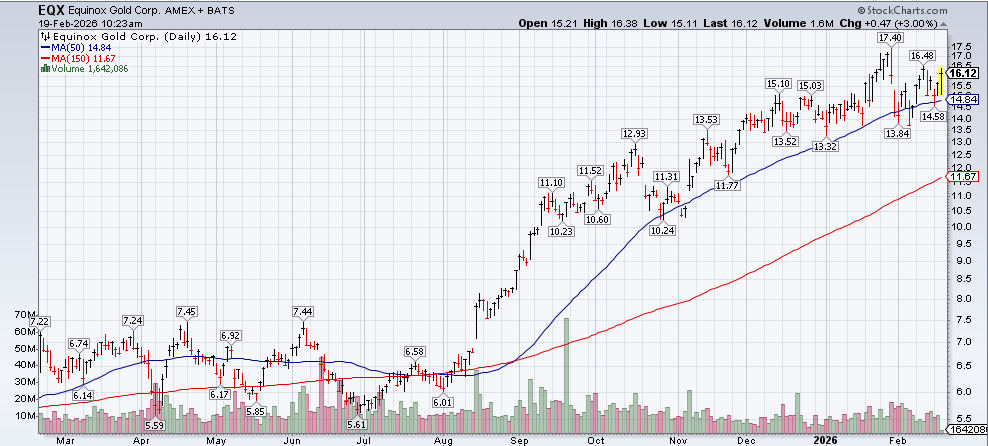

Equinox Gold (EQX) $15.40

Equinox Gold (EQX) released its Q4 and full-year 2025 unaudited financial and operating results on February 18, 2026 (with the conference call/webcast on February 19). This covers the last quarter (Q4 2025) and provides context for their forward outlook.

Quick summary of the last quarter (Q4 2025): The company delivered record quarterly gold production of around 247,000 ounces (including contributions from new assets like Greenstone and Valentine). Revenue figures vary slightly across reports but were strong year-over-year (e.g., in the range of $681M to $819M in different summaries, reflecting significant growth, partly from the Calibre merger and higher gold prices). They reported net income in the $187M–$197M range (with EPS around $0.21–$0.35 adjusted/non-GAAP, showing a beat in some metrics but mixed on others like a slight miss in certain adjusted EPS views). Overall, it capped a transformational year with record full-year production of 922,827 ounces, portfolio optimization (including the sale of Brazil operations), and over $1.1 billion in debt reduction.

Forward-looking projections (focus on next 3–4 quarters in 2026): Equinox Gold provided consolidated 2026 guidance on January 14, 2026 (reaffirmed/updated in recent materials), excluding the divested Brazil operations. The company expects to produce 700,000–800,000 ounces of gold for the full year, at cash costs of $1,425–$1,525 per ounce and all-in sustaining costs (AISC) of $1,775–$1,875 per ounce. This represents a shift to a more streamlined, higher-quality portfolio heavily weighted toward Canada (with an ~80% increase in annual Canadian gold production compared to prior periods).

Breakdown by key assets (site-level guidance for 2026):

- Greenstone (Ontario, Canada): 250,000–300,000 oz, cash costs $1,350–$1,450/oz, AISC $1,750–$1,850/oz. The mine is ramping up toward design capacity (targeting ~330,000 oz/year long-term), with expectations to reach/approach full capacity by mid-2026.

- Valentine (Newfoundland, Canada): 150,000–200,000 oz, cash costs $1,100–$1,200/oz, AISC $1,200–$1,300/oz. Already in commercial production (achieved November 2025), ramp-up to capacity expected in Q2 2026 (long-term target ~175,000–200,000 oz/year). Recent exploration (e.g., Minotaur discovery) supports potential Phase 2 expansion.

- Nicaragua Complex (Limon & Libertad): 200,000–250,000 oz, cash costs $1,750–$1,850/oz, AISC $2,100–$2,200/oz.

- Mesquite (California, USA): 70,000–80,000 oz, cash costs $1,550–$1,650/oz, AISC $2,300–$2,400/oz.

Additional 2026 outlook elements:

- Growth/exploration capital: $325–$375M total (with site-specific allocations, e.g., $130–$160M at Greenstone, $95–$115M at Valentine).

- Exploration budget: $70–$80M company-wide to support resource expansion and discoveries.

- G&A: $80–$90M (excluding share-based comp).

- Broader priorities include generating free cash flow to eliminate remaining debt (net debt already down to ~$75M as of early 2026), self-funding organic growth (potential +400,000–500,000 oz annually over the next 5 years from Valentine Phase 2, Castle Mountain expansion, and Los Filos restart/optionality), and shareholder returns (inaugural quarterly dividend of $0.015/share declared, plus NCIB share buyback program up to ~5% of shares).

Management emphasized strong momentum into 2026 from Canadian assets hitting stride, deleveraging, and high gold prices supporting cash flow generation. Note that guidance may be revised based on operational results, gold prices, or other factors.

For the most precise details, check the official press release or MD&A on equinoxgold.com (audited statements coming later this month).

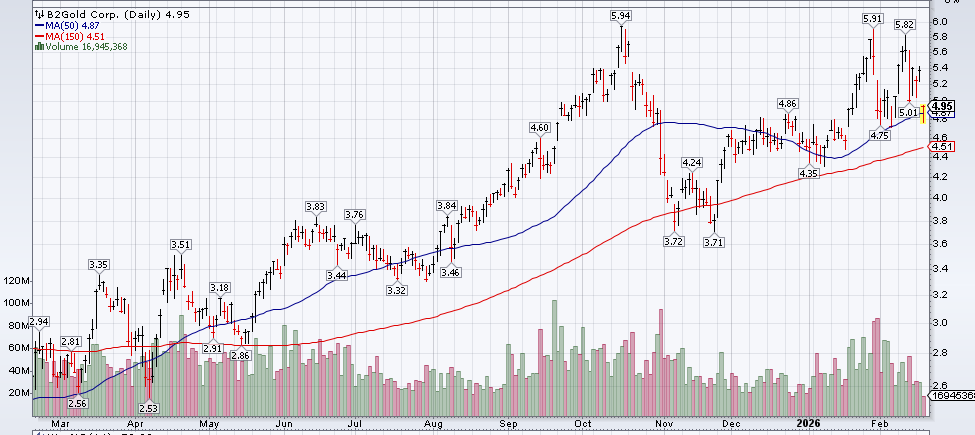

B2Gold (BTG) $4.85

Quick summary of the last quarter (Q4 2025): The company reported gold revenue of $1.05 billion (from sales of about 283,490 ounces at an average realized price of $3,718/oz), with total consolidated gold production around 303,000 ounces. Net income attributable to shareholders was $171 million ($0.13 per share), while adjusted net income was $147 million ($0.11 per share). This adjusted EPS missed analyst expectations (consensus around $0.18–$0.20). Cash operating costs were $736/oz, and all-in sustaining costs (AISC) were $1,754/oz. For full-year 2025, B2Gold achieved record revenue of $3.06 billion (from 927,797 ounces sold at $3,299/oz average), swung to a profit with net income of $402 million ($0.30/share), and met its production and cost guidance.

Forward-looking projections (2026 guidance, covering the next three to four quarters): B2Gold’s 2026 guidance focuses on total attributable gold production of 820,000 to 970,000 ounces. This represents a potential step up from 2025’s ~926,000 ounces (from core operations), driven primarily by the ramp-up of the new Goose Mine in Nunavut (which achieved commercial production in late 2025) and contributions from existing assets like Fekola (Mali), Masbate (Philippines), and Otjikoto (Namibia).

The wide range (820k–970k oz) reflects some uncertainty in the timing and pace of Goose’s ramp-up to full capacity, where costs are expected to drop significantly once stabilized (earlier estimates suggested ~250,000 oz from Goose in 2026, with higher averages in later years). Fekola’s underground operations (approved recently) are set to contribute meaningfully more in 2026 onward, and the Fekola Regional project could add longer-term upside (targeting ~180,000 oz annually from 2026–2029, with B2Gold holding 65% interest).

No specific quarterly breakdowns were provided in the guidance, but production is likely weighted toward the latter half of 2026 as Goose continues ramping and underground at Fekola scales. Cost guidance wasn’t detailed in summaries, but the emphasis is on margin expansion from higher volumes and sustained high gold prices. The company also declared a Q1 2026 dividend of $0.02 per share, maintaining shareholder returns amid a strong balance sheet (cash ~$380 million at year-end 2025).

Overall, the outlook points to growth and improved efficiencies in 2026, though execution on new mine ramp-ups will be key. Shares reacted downward post-release (likely due to the EPS miss overshadowing the guidance and record revenue).

LOTM Considers both EQX and BTG as a buying opportunity for six month to one year holding period. This is not investment advice, just a personal opinion.

LOTM Research & Consulting Service

* An account related to LOTM holds a position in this security.

Neither LOTM nor Tom Linzmeier is a Registered Investment Advisor.

Please refer to our web site for full disclosure at www.LivingOffTheMarket.com ZTA Capital Group, Inc.

To Unsubscribe please select “return” and type Unsubscribe in the subject line..

![]()