Dated April 2nd 2026

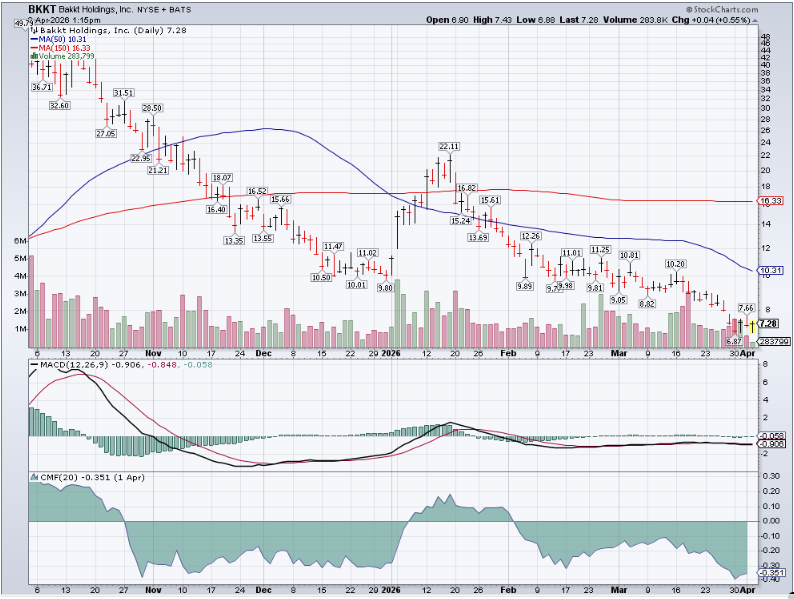

The first time I bought BKKT was in 2021. The stock double within a week of my purchase – and I did not sell any shares. About six-months later I sold the position for a tax loss. The second time I bought, the stock price never rallied and I sold for a losss – smaller that the first go round. The stockcan be volatile and timing is everything! This is the third time – I think it will work. See reasons below.

Based on reports from early 2026, Bakkt Holdings (BKKT) is undergoing a significant transformation from a speculative, diversified fintech into a focused, B2B digital asset infrastructure provider. With our two-year time horizon (2026-2028), the stock is considered a high-risk, high-reward turnaround play.

Actually, I think the risk is modest. They are debt free, have a new and younger Management team with strong digital asset experience. BKKT projects to be profitable in Q2 of 2026.

BAKKT has new CEO in Akshay Naheta. Prior to joining Bakkt in March 2025, he founded Distributed Technologies Research (DTR) in January 2023, a company building the next-generation financial infrastructure focused on programmable finance for businesses and consumers globally. DTR was acquired by Bakkt in January 2026.

They added Lyn Alden to the board of directors—wow, did this surprise me. I love Lyn. She is a no-nonsense thinker who speaks her mind and is right most of the time. They also added Mike Alfred to the board of directors. Mike is a large shareholder of Strive (ASST) & IREN (IREN) also a very straight shooter and very successful self-made entrepreneur. Link to board member bio’s here. Both Mike and Lyn have big followings.

ICE (Intercontinential Exchange) owner of the New York Stock Exchange, owns 27% of BKKT. I also like the fact that they have stock price leverage in that BKKT only has 31 million shares outstanding and no debt. As they say, its hard (but not impossible) to go out of business, if you have no debt. 31 million shares is a small # of shares outstanding for a big market opportunity. Check out EPS projections below.

Here are the pros and cons of owning BKKT based on its 2025-2026 restructuring:

Pros

- Strategic Pivot & Focus: Bakkt has successfully divested non-core assets (loyalty business, custody) to focus on high-growth areas: digital asset trading, payments, and AI-enabled infrastructure.

- Strengthened Balance Sheet: By early 2026, Bakkt reported having eliminated long-term debt and completed capital raises (e.g., $100 million in 2025), aiming for better liquidity to fund operations.

- Potential for Profitability: Following massive cost-cutting and a leaner structure, analysts projected Bakkt could potentially reach breakeven or profitability in the first half of 2026.

- Market Tailwind (Crypto Infrastructure): The company is positioning itself to capitalize on the growing demand for Bitcoin treasury strategies by corporations and stablecoin payments, aiming for institutional-grade clientele.

- Partnerships & Insider Buying: Strategic board appointments and increased insider buying in 2025-2026 suggest confidence from management in the new direction.

Cons

- Extremely High Volatility and Risk: The stock has experienced extreme volatility (beta of 6.1) and is classified as high-risk, frequently trending downwards in the short term.

- Execution Risk: Despite the strategic shift, Bakkt must prove it can onboard new clients to replace lost revenue from major previous partners (like Webull), a challenge that could cause a lag in growth.

- Persistent Cash Burn & Dilution Risk: Despite raising capital, the company has a history of burning through cash, meaning further financing or dilution of shares is possible.

- Intense Competition: Bakkt is competing against established, well-capitalized fintech giants like Stripe and PayPal in the digital payments and infrastructure space.

- Macro Crypto Dependence: While trying to be “infrastructure,” Bakkt’s revenue remains tied to crypto trading volumes, making it vulnerable to “crypto winters”

Bakkt Holdings (BKKT) is projected to turn profitable in the first half of 2026 based on a strategic pivot to a “pure-play” B2B crypto infrastructure provider, significant operational restructuring, and the elimination of non-core, unprofitable business lines. Key drivers include a transition to high-margin software solutions, the acquisition of DTR, and the reduction of legacy operating costs.

Core Reasons for Projected 2026 Profitability:

- Pivot to B2B Crypto Infrastructure: Bakkt has moved away from low-margin/high-cost areas to focus on crypto infrastructure, stablecoin payments, and institutional trading/custody. This includes providing software services (Bakkt Agent) for B2B partners.

- Cost Reduction and Restructuring: The company successfully divested its costly custodial division and exited its legacy loyalty business. By 2026, it is reported that prior-year restructuring costs are “fully behind us”. Q3 2025 already saw a 59% year-over-year reduction in SG&A expenses, leading to positive adjusted EBITDA.

- Acquisition of DTR (Distributed Technologies Research): In January 2026, Bakkt agreed to acquire DTR, which is expected to expand its stablecoin payment capabilities and enhance its position in global digital financial infrastructure.

- Debt-Free Balance Sheet and Cash Management: Bakkt recorded the elimination of long-term debt by late 2025 and raised approximately $100 million in strategic capital, allowing it to enter 2026 with a cleaner financial structure.

- AI-Driven Operational Efficiency: Bakkt implemented “modular tech stack” and “agentic AI” solutions that reported a 98% decrease in response time and a 50%+ increase in engineering efficiency, lowering operational costs.

- Revenue Focus on High-Growth Areas: The company is focusing on high-potential markets like bitcoin treasury strategy for public companies and stablecoin payment rail infrastructure, rather than purely trading volume-based revenue.

- Next earnings (Q1 2026) are expected around early-to-mid May 2026, with some sources citing EPS around -$0.07 to -$0.10 and revenue in the $300M–$570M range (estimates vary across platforms).

- Analyst coverage appears relatively thin or focused on the immediate quarters, which is common for smaller or volatile stocks like BKKT. Full quarterly breakdowns beyond Q2 are not widely published in the sources reviewed.

- FY 2026 revenue consensus is around $2.5 billion in some reports (flattened recently), but EPS remains the primary focus here.

Source finviz

Source finviz

Full Year 2026 EPS Estimate

- Forward guidance for FY 2026: +$0.90 (consensus from MarketWatch)

Recent revisions show improving sentiment for the full year (up from ~$0.55 one and three months ago), while Q1 moved slightly more negative and Q2 moved slightly positive.

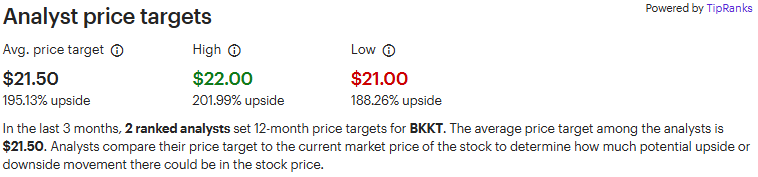

TIPRANK ANALYST TARGETS:

What ever happens to the price of Bitcoin or any of the altcoins, Banks and Traditional Stock Exchanges are rushing at break-neck speed to convert tradition finannce (TradFi) on to crypto/digital infrastructure. BAKKT is one way to participate with Intercontinential Exchange (ICE) as a one of the strongest partners you can find.

Does ICE’s AI and Digital-Asset Push Reshape The Bull Case For Intercontinental Exchange (ICE)?

- In recent days, Intercontinental Exchange, Inc. has rolled out AI-driven mortgage servicing agents, unveiled its ICE Private Credit Intelligence platform with Apollo as anchor partner, advanced new Encompass integrations via Docutech, expanded into container freight futures, and announced a minority investment and collaboration with blockchain firm OKX. Follow headline link for full story.

OKX won’t rush IPO as exec warns poor listings hurt crypto industry

- OKX aims to deliver consistent shareholder returns, even after a $25 billion valuation tied to its deal with Intercontinental Exchange, the parent company of the New York Stock Exchange. Follow headline link for full story.

Forbes Digital Assets

‘Number Goes Up’—Morgan Stanley BTC ETF Has Bulls Targeting $200K

- Morgan Stanley is preparing to launch the cheapest spot Bitcoin ETF on the market and some analysts say it could be the catalyst that sends Bitcoin to six figures and beyond.

- It will be the first spot Bitcoin ETF issued directly by a major U.S. bank.

- What Makes MSBT (Morgan Stanley Bitcoin ETF) Different?

It signals something structural. Morgan Stanley has roughly 16,000 financial advisors managing approximately $9 trillion in client assets. Unlike self-directed brokerage platforms, those advisors can actively recommend Bitcoin allocations to clients. Until now, those advisors couldn’t easily recommend the existing ETFs. Morgan Stanley’s compliance process blocked competitor products. That’s about to change. “MS has 16,000 financial advisors managing $9T,” noted Zack Abrams, a reporter at The Block, citing Bloomberg’s analysis. “Early April launch is eyed. Follow headline link for full story.

Buying a stock idea is only part of turning it into profit. How you manage the position sizing, company risk management tactics, portfolio risk management strategy, and your targeted time-line are on-going work that comes after you buy. Have you defined your exit strategies? We’re looking for a double from BAAKT in one to two-years time-line with a dollar-cost-averaging (DCA) accumulation strategy.

Important Notice Regarding BKKT Shares

DO NOT PURCHASE BAKKT SHARES IF ILLIQUIDITY and/or VOLATILITY ARE NOT APPROPRIATE FOR YOU!

Investors should be aware that BAKKT shares may experience periods of illiquidity and significant volatility. These characteristics can impact the ability to buy or sell shares efficiently and may result in substantial price fluctuations. It is essential to carefully consider your risk tolerance and investment objectives before deciding to invest in BAKKT shares. If you are uncomfortable with the potential for illiquidity or volatility, it is advised not to proceed with purchasing these shares.

I believe BAKKT shares have potential 2X to 4X over the next 18 to 36-months but you know very well we are dealing with probabilities and hope that does not always work out.

LOTM Working to make your returns better.

LOTM Research & Consulting Service

* An account related to LOTM holds a position in this security.

Neither LOTM nor Tom Linzmeier is a Registered Investment Advisor.

Please refer to our web site for full disclosure at www.LivingOffTheMarket.com ZTA Capital Group, Inc.

To Unsubscribe please select “return” and type Unsubscribe in the subject line..

![]()