- Galaxy Digital (GLXY) $20.59

- CoinShares (CNSRF) $8.10

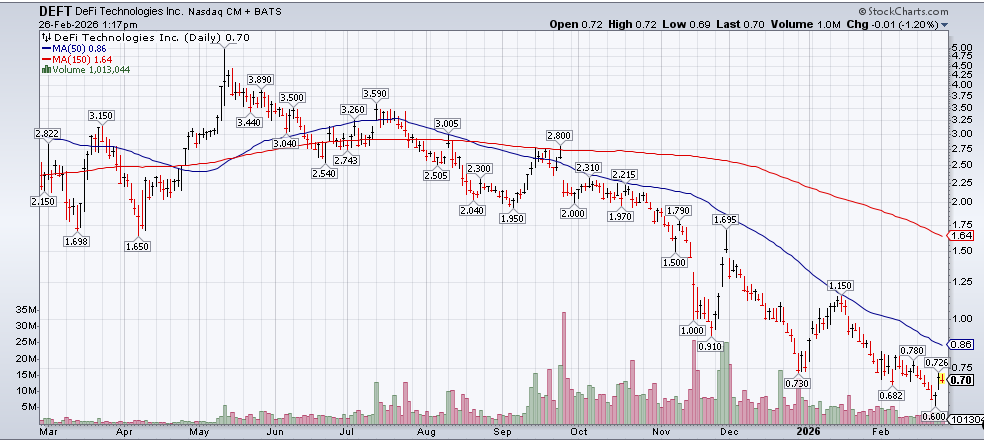

- DeFi Technologies (DEFT) $0.68

Comparative features of the Asset Management Divisions

The division that each of the companies share in common is their Crypto Asset Management division. Therefore, we thought it helpful to shares these operations as a starting point.

As of early 2026, Galaxy Digital (GLXY) remains the largest Crypto Asset Manager of the three by total assets, while CoinShares (CNSRF) maintains a dominant European presence, and DeFi Technologies (DEFT) is the fastest-growing in terms of product variety.

Asset Management Division Comparison (FY 2025)

| Metric | DeFi Technologies (DEFT) | CoinShares (CNSRF) | Galaxy Digital (GLXY) |

| AUM | ~$989 Million (Q3 ’25) | $7.4 Billion (Year-End ’25) | $12 Billion (Total Platform) |

| Product Focus | 100+ Digital Asset ETPs (Valour) | European ETPs & Physical ETPs | Institutional Alternatives, ETFs & Staking |

| Key Revenue | Staking & Management Fees | AM Fees & Capital Markets | AM & Infrastructure Solutions |

| 2025 Growth | $138.2M Net Inflows (Record) | $662M Net Inflows (H2 ’25) | $2.0B Net Inflows (AM only) |

Division Highlights

DeFi Technologies (DEFT)

- Operational Arm: Operates primarily through Valour, which reached a milestone of 102 listed ETPs by the end of 2025.

- Performance: Reported record annual net inflows of $138.2 million for 2025, maintaining positive inflows every month despite market volatility.

- Monetization: Generates a blended yield of 5% to 7% through management fees and staking.

CoinShares (CNSRF)

- Operational Arm: Known for its CoinShares Physical and XBT Provider platforms.

- Strategic Expansion: Achieved the first continental European MiCA authorization for its French subsidiary, enabling EU-wide institutional portfolio management.

- Profitability: Reported a 2025 net profit of $32.4 million for Q2 alone, with asset management fees reaching $30 million that quarter.

Galaxy Digital (GLXY)

- Operational Arm: Asset Management & Infrastructure Solutions (GAM). Its $12 billion on-platform assets include $6.4 billion in AUM and $5.0 billion in Assets Under Stake.

- Institutional Strength: Secured major multi-year mandates from digital asset treasury companies, adding over $4.5 billion to its platform.

- Revenue Model: Transitioning toward a data center infrastructure model (Helios campus) alongside its legacy crypto business, expecting over $1 billion in annual revenue from 2026 onward

Past Company Operational Performance:

Financial performance for Galaxy Digital, DeFi Technologies (DEFT), and CoinShares (CNSRF) varies significantly due to their distinct operational focuses within the digital asset sector. Galaxy Digital operates a massive-scale institutional platform, DeFi Technologies focuses on high-growth ETPs and arbitrage, and CoinShares maintains a leading position in the European ETP market.

Financial Performance Comparison (2025/2026)

| Metric | Galaxy Digital (GLXY) | DeFi Technologies (DEFT) | CoinShares (CNSRF) |

| Annual Revenue | ~$61.36B (2025) | ~$116.6M (2025 Forecast) | ~$40M (Q1 2025 Total) |

| Revenue Growth | 44% (YoY 2025) | 62.1% (Avg Annual Rate) | ~21% (Asset Mgmt Fees YoY) |

| Net Income | -($241M) (2025 Loss) | $17.4M (Q2 2025 Adj.) | $23.8M (Q1 2025 Profit) |

| Profit Margin | -0.39% (GAAP) | 12.6% (Net Margin) | ~59.5% (Q1 2025 Net/Total) |

| Total Equity | $3.0B | $81.5M (Q1 2025 Total Val) | Not Specified |

Company Operations and Growth Rates

Galaxy Digital (GLXY)

Galaxy Digital reported substantial revenue growth in 2025, reaching $61.36 billion, a 44% increase year-over-year. Despite this scale, the company reported a GAAP net loss of $241 million for 2025, largely due to lower digital asset prices and $160 million in one-time costs related to restructuring and mining infrastructure.

- Segment Performance: The Digital Assets segment generated a record adjusted gross profit of $505 million (67% YoY growth).

- Balance Sheet: Total equity increased 38% YoY to $3.0 billion, supported by $2.6 billion in cash and stable coins.

- Growth Drivers: Strong contributions from Trading, Lending, and Asset Management. Its average loan book expanded to $861 million by the end of 2024.

DeFi Technologies (DEFT)

DeFi Technologies has experienced rapid, albeit volatile, expansion. Its revenue grew from $7.84 million to $38.37 million in 2024. However, the company recently lowered its full-year 2025 revenue guidance from $218.6 million to $116.6 million due to compressed arbitrage spreads and market consolidation.

- Margins: The company maintains a net margin of 12.6% and an average annual earnings growth rate of 17.3%.

- Balance Sheet: Bolstered by a $100 million equity financing in late 2025. As of March 2025, it held $81.5 million in total cash, digital assets, and venture portfolio value.

- Growth Drivers: Assets Under Management (AUM) for its Valour business reached $989.1 million as of September 2025.

CoinShares (CNSRF)

CoinShares maintains strong profitability with a focus on asset management fees. In Q1 2025, it reported a net profit of $23.8 million on total revenue/gains of $40 million.

- Asset Management Growth: Revenue from asset management fees grew to $29.6 million in Q1 2025, up from $24.5 million in Q1 2024.

- AUM Status: Total gross AUM was $7.40 billion at the end of 2025, down from a peak of $10 billion due to price weakness in Q4.

- Growth Drivers: The company is expanding into the U.S. market through a proposed $1.2 billion business combination with Vine Hill Capital Investment Corp.

Compound Annual Growth Rate (CAGR) Comparisons

Direct multi-year CAGR figures are influenced by extreme volatility in digital asset markets:

- DeFi Technologies: Reported an average revenue growth rate of 62.1% per year and earnings growth of 17.3% over the past five years.

- Galaxy Digital: Exhibits high volatility; for example, it saw a 753% revenue increase in 2021 followed by significant declines and a subsequent 44% recovery in 2025.

- CoinShares: Has seen its AUM more than triple over the last two years, with its Physical ETP platform achieving 5.4x revenue growth from 2023 through Q2 2025.

- Current analyst projections for Galaxy Digital (GLXY), DeFi Technologies (DEFT), and CoinShares (CNSRF) through February 2029 suggest significant but varying degrees of potential appreciation. While all three are tied to the digital asset market cycle, DeFi Technologies currently holds the highest consensus upside percentage from current price levels, whereas Galaxy Digital offers a more diversified institutional-grade model with a lower projected percentage gain but higher absolute price targets.

3-Year Potential Appreciation Comparison

| Metric | Galaxy Digital (GLXY) | DeFi Technologies (DEFT) | CoinShares (CNSRF) |

| Current Price | ~$20.55 | ~$0.68 | ~$8.10 |

| Avg. 1-Year Target | $44.94 (+108%) | $3.55 – $4.50 (+400-580%) | $17.86 (+123%) |

| 2027 Outlook | ~$34.96 (+60%) | Consensus ~$4.25 (+500%) | Growth in tokenized assets. Target market growth to $30T by 2034 |

| 2028-29 Target | $34.83 – $60.00 | Highly variable; model-based up to $8.87 | N/A |

Analysis of Key Growth Drivers

- DeFi Technologies (DEFT): Analysts highlight the highest potential for explosive growth, with some consensus targets reaching $4.50—a roughly 580% upside from current levels. This is driven by their expansion in digital-asset ETPs and the potential for a market reset after a sharp decline in early 2026.

- Galaxy Digital (GLXY): As a more established player, its 3-year outlook is bolstered by a massive 1.6 GW data center strategy and its role in institutional tokenization. While the price is expected to double to ~$45 within the next year, long-term models see it fluctuating between $34 and $60 by 2028, depending on its ability to execute on its Bitcoin mining and infrastructure contracts.

- CoinShares (CNSRF): Positioned as a value play with a low P/E ratio of ~4.02. One-year targets suggest an appreciation to $17.86 (+155% from recent lows). Its long-term potential is tied to the tokenized asset market, which it projects could reach trillions by the end of the decade.

Risk Factors to Consider

- Volatility: All three stocks show high correlation with underlying crypto-asset prices; sudden market downturns (like those seen in Q4 2025) can lead to swift pullbacks regardless of long-term targets.

- Execution: Galaxy’s infrastructure plans require heavy capital expenditure through 2028, while DeFi Technologies’ valuation relies on maintaining its aggressive ETP inflow momentum.

Valuation Multiples Comparison

- Galaxy Digital (GLXY): Currently trades at a Forward Price/Sales (P/S) of 0.08x for 2026, which is significantly lower than the industry median of 2.6x. Despite recent negative EPS due to heavy infrastructure spending (data centers), its Price/Earnings (P/E) is projected to stabilize as it scales its 1.6 GW mining strategy.

- DeFi Technologies (DEFT): Exhibits a Forward P/E of 4.22x to 4.84x for 2026, reflecting high investor expectations for its ETP (Exchange Traded Product) inflows. Its P/S ratio sits around 3.62x, suggesting it is valued more as a high-growth tech platform than a traditional financial firm.

- CoinShares (CNSRF): Positioned as the “value” play of the group with a trailing P/E of 4.02x. While revenue growth is steady at ~12% per annum, analysts forecast a slight decline in EPS (-5%) as margins compress in the competitive European ETP market.

Strategic Outlook by 2028

- Galaxy Digital is transitioning from a merchant bank to a Bitcoin infrastructure giant, with its 2028 revenue targets tied to massive long-term hosting contracts.

- DeFi Technologies is banking on “Hybrid Finance”—the convergence of on-chain yields with regulated products—to drive its 50% annual earnings growth.

- CoinShares focuses on institutional integration, projecting that the tokenized asset market will reach $3 trillion by 2030, which would provide a significant tailwind for their asset management fees.

Key “Smart Money” Trends

- Galaxy Digital: The Institutional Choice

Galaxy has the most “blue chip” backing, with 358 institutional owners. The aggressive stake increases by BlackRock and Invesco suggest high confidence in Galaxy’s role as a primary institutional on-ramp and infrastructure provider for the next three years. - DeFi Technologies: Insider Conviction

While institutional ownership is lower (12%), the high frequency of insider purchases by the C-suite in early 2026 (averaging prices between $0.72 and $0.88) often signals that management believes the stock is significantly undervalued relative to upcoming growth. - CoinShares: Awaiting a Catalyst

CoinShares is currently the least “liquid” for institutions due to its OTC status and concentrated insider ownership. However, the pending merger and U.S. listing (expected end of Q1 2026) is the intended catalyst to attract the same institutional inflows currently seen in Galaxy.

This report comprised from of a consolidation of public information available on the internet. Some of the data might be dated or based on opinion of others. Accounts related to LOTM holds a position in Galaxy Digital and one of CoinShares ETFs, symbol DIME in the US NASDAQ exchange.

Charts dated 2/26/26

#galaxydigital #defitechnoglies #coinshares #stocks #crypto #stockideas

LOTM Research & Consulting Service

* An account related to LOTM holds a position in this security.

Neither LOTM nor Tom Linzmeier is a Registered Investment Advisor.

Please refer to our web site for full disclosure at www.LivingOffTheMarket.com ZTA Capital Group, Inc.

To Unsubscribe please select “return” and type Unsubscribe in the subject line..

![]()