MNR* (MACH Natural Resources) $12.50

Recent quarterly dividend annualized is 8.64%

MACH Natural Resources pays a Variable quarterly distribution.

MACH has reduced its quarterly distribution to allow acquistions and the expenses related to the purchases and integeration of said acquistions. It is anticipated and projected by management that dividend would increase at some time in 2026 to a goal of around $2.00 annually.

MNR (MACH Natural Resources) $12.46 – 11% projected dividend

For a three-year holding period, investing in Mach Natural Resources (MNR) offers potential upside from its focus on natural gas, recent acquisitions, and improving capital efficiency, along with an attractive dividend yield. However, it comes with significant risks, including exposure to volatile natural gas prices, integration challenges from recent acquisitions, and potential negative impacts from hedging strategies and a notable decline in oil production.

Pros of investing in Mach Natural Resources for a three-year holding period

- Positive growth outlook and production shift: The company is strategically shifting its focus towards natural gas development in the Anadarko and San Juan basins, which is expected to drive production growth. Management projects natural gas volumes to exceed 70% of production by the end of 2026, benefiting from a currently favorable natural gas price environment.

- Accretive acquisitions: Recent large acquisitions, including the IKAV and Sabinal deals, are expected to be accretive to cash available for distribution. They are projected to boost it by 8% in the first year and 28% by the fifth year. These deals also contribute to the company’s overall production increase, despite a decline in oil output.

- Strong balance sheet: Despite recent acquisitions, the company maintains a conservative balance sheet, with a net debt-to-Adjusted-EBITDA ratio of 1.0x as of December 31, 2024. Management is committed to keeping this metric low and has implemented an 8% reduction in the 2026 capital expenditure budget, signaling fiscal discipline.

- Attractive variable distributions: The company employs a variable distribution framework, adjusting payments based on commodity cycles and cash generation. While recent distributions have been lower due to one-time costs, higher payments are anticipated in future quarters as acquired assets are integrated and deal costs subside.

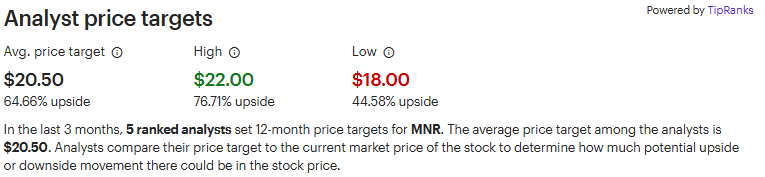

- Undervalued stock potential: Analyst valuations, particularly using discounted cash flow (DCF) models, have suggested the stock could be significantly undervalued. For instance, a November 2025 analysis suggested a potential 72% upside.

Cons of investing in Mach Natural Resources for a three-year holding period

- Significant exposure to natural gas prices: The company’s increased focus on natural gas production makes it highly sensitive to fluctuations in natural gas prices. A sustained period of low natural gas prices could negatively impact earnings, cash flows, and distributions.

- Declining oil production: Mach Natural Resources is actively reducing its oil production in favor of natural gas. This could hurt revenue as oil typically commands a higher price per barrel of oil equivalent (BOE) compared to natural gas, even with recent improvements in gas prices. LOTM Comment: Doomberg, a recoginzed energy expert, believes Nat Gas will be the premium fuel and Oil a By-product of Nat Gas – flipping the logic presented here. (Doomberg comment at 20 minute mark of this interview).

- Operational and market volatility risks: The oil and gas sector is inherently volatile and subject to market fluctuations, regulatory changes, and environmental scrutiny. These factors can impact the company’s performance, earnings stability, and hedging strategy effectiveness.

- Negative free cash flow: While analysts forecast positive free cash flow in the future, the company recorded negative free cash flow in the trailing 12 months as of late 2024, partly due to high capital expenditures. This could be a concern for investors prioritizing immediate cash generation.

- Integration and execution risks: Recent acquisitions introduce integration risks. The successful realization of projected synergies and sustained high production and distributions depend on management’s execution of integration plans and operational efficiency.

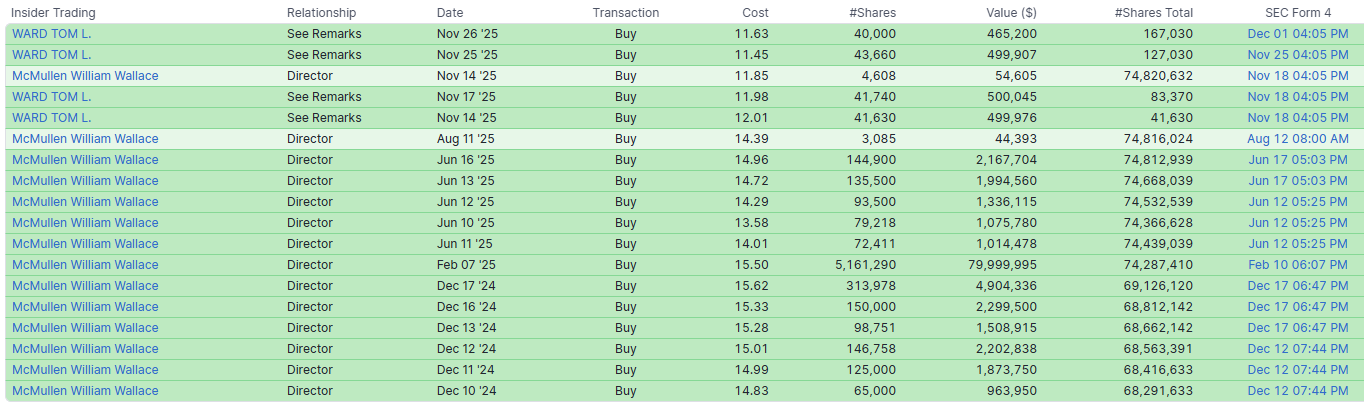

MNR Insider Buying.

The size of the orders is note worthy

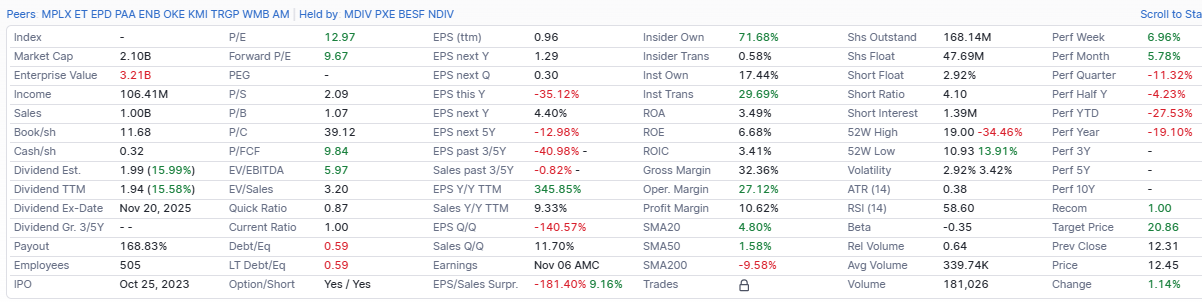

MNR Stats Page @ Finviz.com

Consolidated 2025 and 2026 Distribution Projections from mutiple sources:

- Q4 2025: Management anticipates higher distributions than the $0.27 per unit paid for Q3 2025. This is due to one-time deal-related costs from its recent IKAV and Sabinal acquisitions no longer impacting cash flow.

- 2026: Analysts project approximately $0.48 to $0.49 per quarter in distributable cash flow at current strip prices. However, actual distributions might be lower, as some of this cash will likely be used to reduce debt and bring the company’s leverage ratio down towards its target of 1.0x. The company is projected to generate $1.94 per unit in distributable cash flow for the year, but may only distribute around $0.35 per quarter while allocating the rest towards debt repayment.

- Post-2026 (Mid-Cycle Gas Prices): Should natural gas prices remain favorable, the sustainable distribution rate could be higher, potentially exceeding $2 per unit annually.

LOTM projects 10% plus annual distribution with price upside of 50% to 70%. If Management hits its goal of about $2.00 annual distribution, by the 4th quarter of 2026, the cash distribution in the last two-years of the three-year hold would be 16% annual rate on a $12.50 cost.

LOTM Research & Consulting Service

* An account related to LOTM holds a position in this security.

Neither LOTM nor Tom Linzmeier is a Registered Investment Advisor.

Please refer to our web site for full disclosure at www.LivingOffTheMarket.com ZTA Capital Group, Inc.

To Unsubscribe please select “return” and type Unsubscribe in the subject line.

![]()